How findings from our 10-year market forecast reflect real-world trends in the private jet market

The annual NBAA-BACE trade show is defined by one thing – an industry-wide interest in, and passion for, aviation.

Which is why Aerion’s announcement – that the first transatlantic supersonic jet since Concorde would soon be taking to the skies – was greeted with such enthusiasm at this year’s show. Aerion announced that the jet is on track to fly in June 2023, with the first transatlantic crossing the same year, 20 years after the celebrated Concorde flew its last.

Click to Enlarge

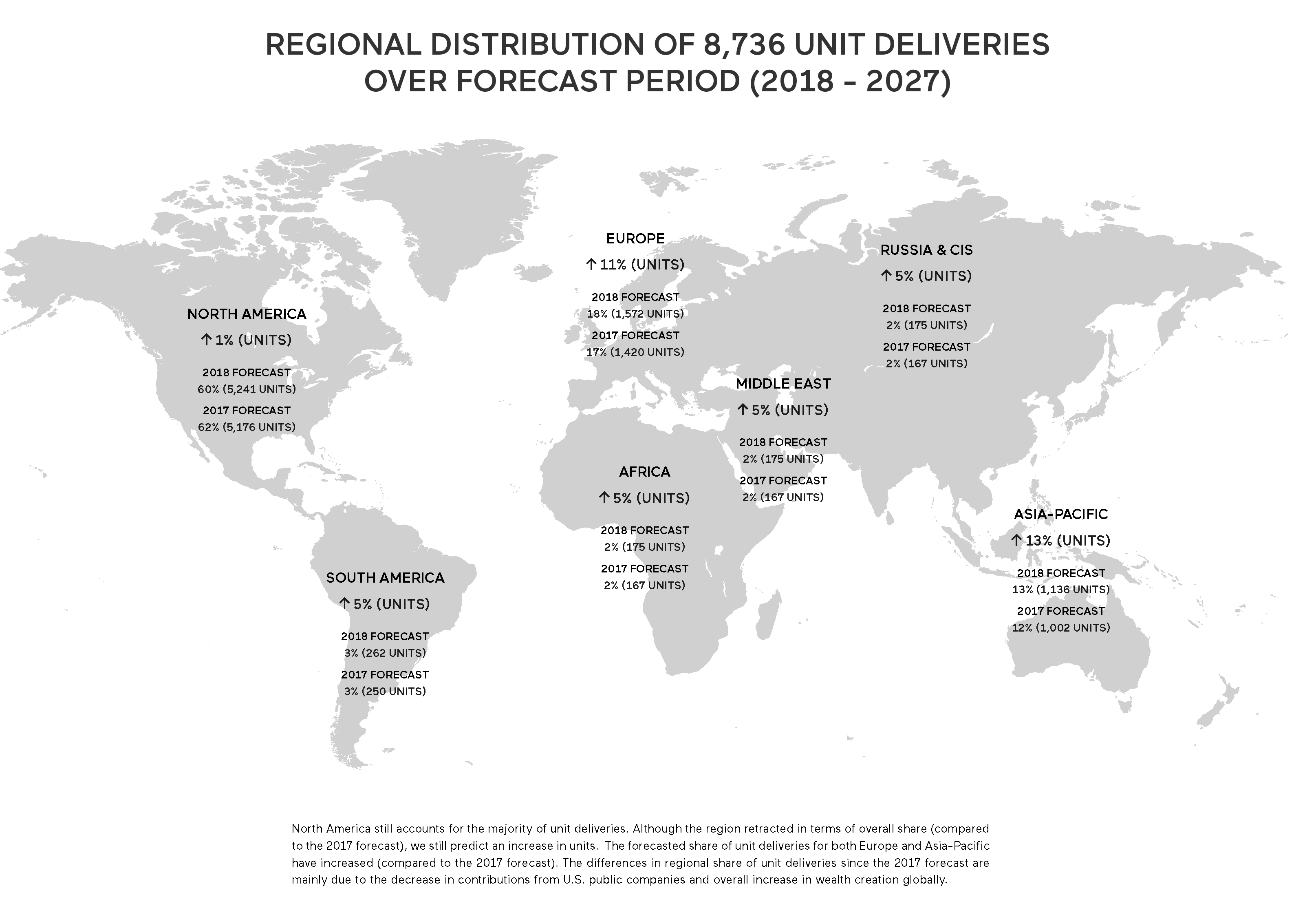

The faster-than-sound business jet will undoubtedly be a market disruptor, particularly given its anticipated intercontinental capabilities, which will be a key indicator of its market performance. According to Jetcraft’s new 10-year market forecast, those regions where business needs are increasingly globalized will take the lead in terms of unit deliveries. North America is set to account for 60% of deliveries (5,241 units) over the forecast period, with Europe taking second place at 18% (1,572), and Asia Pacific third at 13% (1,136).

Looking beyond new models to the pre-owned market, inventory levels are finally back to pre-recession levels, resulting in an increase in market competitiveness – and often more than one buyer for each aircraft. Some of the best deals are now made before an aircraft is even advertised. So, for both buyers and sellers, the need has never been greater to work with a consultant that has inventory visibility and can provide up-to-the-minute market insight.

It’s important to note, however, that buyer profiles have shifted slightly. Our analysis shows that some Fortune 500 companies have yet to return to historical aircraft transaction levels, as businesses are focusing on other financial priorities, such as share buybacks and paying down debt. This means they may not jump back into purchasing aircraft as quickly as we would have hoped.

Nevertheless, we anticipate that the increase in individual buyers will more than offset this. Worldwide wealth creation has spurred growth in family offices that are now offering a wide variety of specialized services, including business aviation. Together with the increase in block charter and fractional programs, this is exposing more ultra-high net worth individuals to the industry than ever before.

The lessons learnt in the industry over the past decade, since the economic downturn, have meant a slow return to optimism. But we’re confident that these lessons will ensure sustainable growth in business aviation for years to come, which is reflected in our 10-year market forecast. Ours is an enduring industry, and one with a buoyant future ahead.

Highlights

How findings from our 10-year market forecast reflect real-world trends in the private jet market

The annual NBAA-BACE trade show is defined by one thing – an industry-wide interest in, and passion for, aviation.

Which is why Aerion’s announcement – that the first transatlantic supersonic jet since Concorde would soon be taking to the skies – was greeted with such enthusiasm at this year’s show. Aerion announced that the jet is on track to fly in June 2023, with the first transatlantic crossing the same year, 20 years after the celebrated Concorde flew its last.

The faster-than-sound business jet will undoubtedly be a market disruptor, particularly given its anticipated intercontinental capabilities, which will be a key indicator of its market performance. According to Jetcraft’s new 10-year market forecast, those regions where business needs are increasingly globalized will take the lead in terms of unit deliveries. North America is set to account for 60% of deliveries (5,241 units) over the forecast period, with Europe taking second place at 18% (1,572), and Asia Pacific third at 13% (1,136).

Looking beyond new models to the pre-owned market, inventory levels are finally back to pre-recession levels, resulting in an increase in market competitiveness – and often more than one buyer for each aircraft. Some of the best deals are now made before an aircraft is even advertised. So, for both buyers and sellers, the need has never been greater to work with a consultant that has inventory visibility and can provide up-to-the-minute market insight.

It’s important to note, however, that buyer profiles have shifted slightly. Our analysis shows that some Fortune 500 companies have yet to return to historical aircraft transaction levels, as businesses are focusing on other financial priorities, such as share buybacks and paying down debt. This means they may not jump back into purchasing aircraft as quickly as we would have hoped.

Nevertheless, we anticipate that the increase in individual buyers will more than offset this. Worldwide wealth creation has spurred growth in family offices that are now offering a wide variety of specialized services, including business aviation. Together with the increase in block charter and fractional programs, this is exposing more ultra-high net worth individuals to the industry than ever before.

The lessons learnt in the industry over the past decade, since the economic downturn, have meant a slow return to optimism. But we’re confident that these lessons will ensure sustainable growth in business aviation for years to come, which is reflected in our 10-year market forecast. Ours is an enduring industry, and one with a buoyant future ahead.

SIGN UP FOR OUR MONTHLY JETSTREAM RECAP

Don't miss future Jetstream articles. Sign up for our Jetcraft News mailing list to receive a monthly eblast with links to our latest articles. Click to join the 1,800+ subscribers on our mailing list.